Fed minutes may elaborate on coming rate cut debate

Precisely when the Federal Reserve will start cutting interest rates stands as the big unknown for markets and economists as 2024 kicks off, and fresh details about its pivot in that direction may emerge from Wednesday’s readout of the last policy meeting of 2023.

Fed officials at their meeting in mid-December held the policy interest rate steady in the range of 5.25% to 5.5%, but issued projections showing most officials expect it would need to fall over the year by at least three quarters of a percentage point as inflation steadily declined to the Fed’s 2% target.

But the year-end projections leave the timing about any initial rate cut in doubt, and Fed Chair Jerome Powell at his press conference following the meeting insisted that was not yet a live topic of discussion.

Investors eager to see the Fed move swiftly to bring down borrowing costs now broadly expect a first rate cut in March, market pricing of contracts tied to the Fed policy rate shows. Economists on balance see the Fed holding off until closer to mid-year.

Minutes of the Dec. 12-13 meeting, scheduled for release at 2 p.m. EST, may give insight on just how close officials feel they are to the point where monetary policy needs to be less restrictive in order to keep a hoped-for “soft landing” on track, with inflation continuing to fall without a major blow to the job market.

“The directionality for the Fed is clear as falling inflation is pushing it toward a rate cut,” wrote SGH Macro Advisors Chief U.S. Economist Tim Duy, who noted that the combination of slowing inflation and a steady federal funds rate means that monetary policy is in effect becoming more restrictive even as inflation eases and employment growth is expected to slow.

Though he said the minutes are “unlikely to directly point” to the March rate cut currently expected by investors, “I suspect they will reveal the Fed becoming increasingly confident that inflation is on a path to price stability.”

In fact, data issued since the Fed’s meeting, and effectively anticipated by policymakers at their Dec. 12-13 session, took a strong turn in that direction.

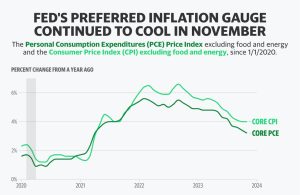

The headline personal consumption expenditures price index for November fell; excluding volatile food and energy costs the “core” rate of inflation rose less than 1% on an annualized basis. Over the six months from June through November, a time frame Fed officials have pointed to as helpful in shaping their policy debate, core PCE inflation has been slightly below the 2% target – a fact some analysts note may push the Fed towards rate reductions sooner than later.

Powell noted at his last press conference that rates would need to fall before inflation returns to the 2% target because otherwise “it’d be too late,” and policy would be more restrictive – and the risks to the job market greater – than necessary.

In an analysis of Fed policy scenarios for the year, Deutsche Bank economists said they felt as a baseline the Fed would begin reducing rates in June, but that if inflation data is weaker than expected “a first rate cut as early as March would be reasonable.”

Investors in contracts tied to the Fed’s policy rate currently put about an 80% probability on a March cut, according to data from the CME Group’s FedWatch tool, with the Fed ultimately cutting the rate 1.5 percentage points by the end of the year – twice what Fed policymakers anticipate.

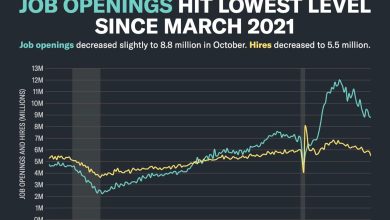

Upcoming jobs and inflation data will shape the eventual outcome, with new job openings data also released Wednesday, a December employment report due Friday, and December consumer inflation data out next week.

The Fed next meets on Jan. 30-31.